RUNNING HOT

By Rob McNeil - Director.Much like our national football players at the World Cup, US refiners are running hot.

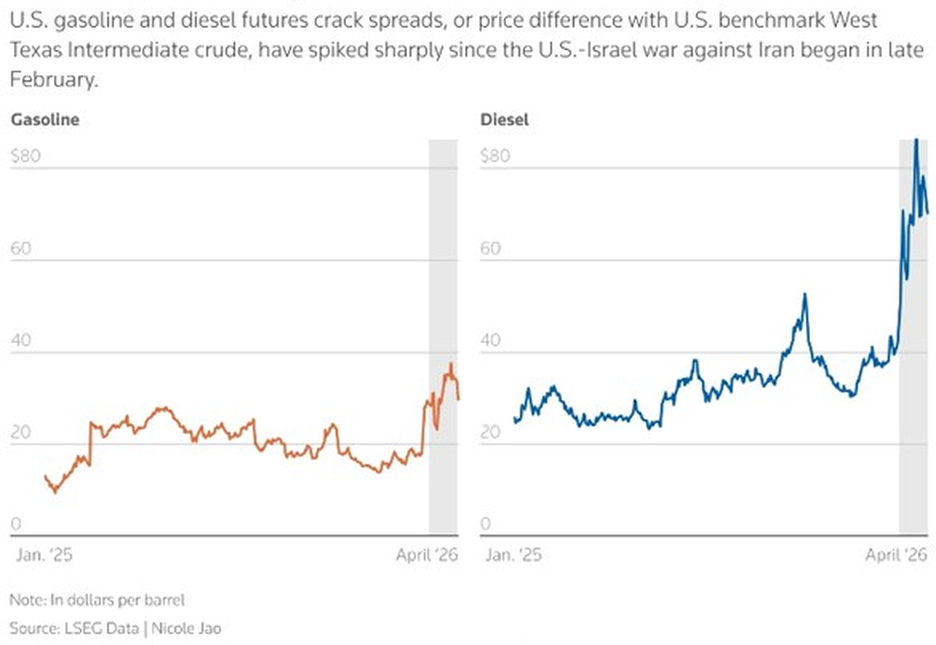

Crack spreads on diesel and gasoline are at extreme seasonal highs, demanding peak utilisation rates for US refiners.

This presents some key insurance challenges, both in terms of a shift in risk and potential coverage.

US refining margins have spiked to near-record levels, driven by a surge in global demand and severe supply disruptions stemming from the Iran war and the blockage of the Strait of Hormuz. With U.S. plants running at over 94% utilisation, this windfall has enabled major refiners to post massive profit increases.

These levels are set to continue over Q3 2026, as the U.S. heads into a season of high domestic demand (particularly for gasoline), further increased by the FIFA World Cup travel.

Drivers for record margins

The increase in refinery production and revenues following the Iran war is driven by a combination of supply disruptions, geopolitical uncertainty, and changing market dynamics rather than by higher crude oil prices alone. Military conflict in the Middle East has disrupted oil transportation routes, particularly through the Strait of Hormuz, one of the world’s most important maritime chokepoints for energy exports. As shipments of crude oil and refined fuels become more difficult and expensive to transport, global markets have experienced tighter supplies and increased price volatility. At the same time, some refining facilities and export terminals within the region face operational interruptions due to security concerns or direct damage, further reducing the availability of finished petroleum products.

US refined product margins soared as Iran war chokes supply

These constraints have caused the prices of refined products to rise faster than the cost of crude oil, significantly widening refining margins, or “crack spreads”. For refineries operating outside the conflict zone and with secure access to crude supplies, particularly those in the US, this has created a highly favourable economic environment in which each barrel of oil processed generates substantially greater profit than under normal market conditions. Consequently, many US refiners have responded by operating at higher utilisation rates, increasing exports to regions experiencing shortages, and adjusting their product mix toward fuels with the strongest demand and highest margins.

Higher refining margins have translated directly into stronger financial performance for refining companies. Several major U.S. refiners have reported earnings that exceeded market expectations, largely due to improved margins rather than increased crude prices alone.

The impact on risk

Periods of sustained high refining margins often encourage operators to maximise throughput and delay planned downtime in order to capture additional revenue. While this strategy can improve short-term profitability, it also has implications for operational risk, which the insurance market needs to be aware of.

Refineries are complex facilities designed to operate continuously, but running at or near maximum capacity for extended periods can place additional stress on critical equipment. Pumps, compressors, heat exchangers, furnaces, pressure vessels and piping systems may experience accelerated wear.

High utilisation can also leave less flexibility to respond to process upsets, increasing the likelihood that minor issues escalate into more significant incidents if not managed effectively.

Routine maintenance, inspections and safety-critical activities are generally governed by strict regulatory requirements and recognised engineering standards.

However, history shows that during periods of exceptionally strong margins, companies may seek to optimise production. Such decisions are typically subject to risk-based inspection programmes and management approval rather than being made solely for commercial reasons.

From an insurance perspective, this issue is particularly important. A prolonged period of elevated utilisation may not immediately increase claims frequency, but the risk shifts if it coincides with deferred maintenance, ageing infrastructure or reduced turnaround durations.

The impact on insured values and claim settlements

Increased profits also raise important considerations for business interruption insurance, particularly in relation to declared insured values and the application of volatility clauses.

Refining margins in some cases are 200% of pre-war levels, with profits increased substantially. In the event of an unplanned shutdown and claim, the business interruption loss can significantly exceed the declared figures in the policy, and policy limits may be exhausted before the business has fully recovered.

The impact on business interruption losses may also be exacerbated due to supply chain constraints for replacement parts, driven by the conflict’s affect on logistics, as well as the fact that a significant amount of manufacturing capacity is being used up to reinstate numerous affected refineries in the conflict zone. The result of this constraint is likely to men increased unit prices for parts, but more significantly extended lead times and overall outage periods.

Volatility clauses are not designed to absorb unlimited changes in exposure and the levels currently being observed in the US are certainly above the typical 10% or 20% variance. Depending on the specific mechanism in a policy, without review of the declared values, a claim is likely to result in significant uninsured exposure for refiners, leading to longer, more difficult claim settlements.

If you would like to discuss ComplexClaims downstream energy claims, get in touch with Rob McNeil or Adam Humphrey:

Rob McNeil rmcneil@complexclaims.partners

Adam Humphrey ahumphrey@complexclaims.partners