Impact of ME events on Insurers

Impact of Middle East events on Insurers

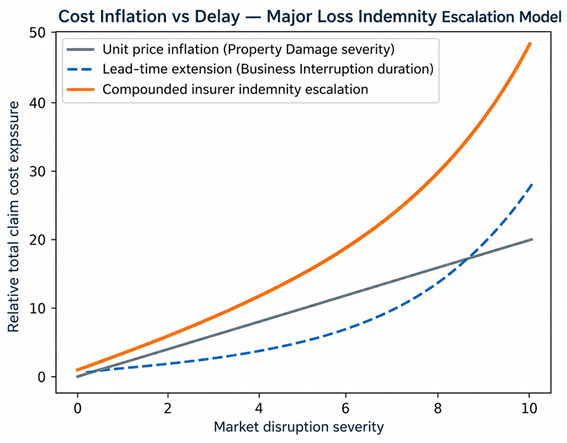

In complex claims, delay driven “timeline” escalation often exceeds pure rebuild cost inflation.

The ongoing conflict, oil price spikes and continuing uncertainty is leading to speculation as to what might all this mean for the world economy. In part, that depends on what happens to the shipments of oil and gas from the region and the scale of long-term damage to oil and gas facilities.

The Financial Times (11 March 2026) reports that Capital Economics considers three scenarios:

1. A short, sharp conflict, lasting about two weeks. They estimate is of a loss of around 1.4 per cent of global annual oil exports and a similar proportion of LNG exports.

2. A conflict lasting three months, but with limited longer-term damage to facilities. The estimate for this is of a loss of 5-6 per cent of world exports of crude and LNG in 2026.

3. A conflict lasting three months, but with longer-lasting damage to capacity, notably to Iran’s Kharg Island. The estimate here is of a loss of 8-9 per cent of world exports of oil and LNG, with an impact into 2027. Oil prices could hit $150 a barrel and gas prices in the EU (per megawatt hour) could hit €120. According to Capital Economics, the only comparable global supply shock to this last possibility was “from the late-1970s to the mid-1980s”.

What are the impacts for Insurers?

This prompts us to ask what are the implications for the insurance claims that we are managing, both within the Middle East region, and more generally?

During the time of the Ukraine and associated energy supply impact in 2022, our claims data demonstrated structural steel prices increasing by more than 300%. This appeared to be Insurers’ primary focus at the time. Indeed, in the current situation, price spikes are already impacting indemnity costs and Insurers’ exposures. But:

____________________________________________________________________________________________

our cost data highlighted that insurers' greater exposure at that time was “time inflation”

____________________________________________________________________________________________

“Time” inflation refers to supply chain challenges (longer procurement lead times, logistics issues, disruption to labour resourcing), leading to greater time element exposures. In 2022, we observed procurement lead times increasing, in some cases, from three to ten months. Insurers, especially those with time element exposures, were far more impacted by this than unit price inflation, in two ways:

(a) Increased time element exposures and time related repair costs (prelims, standing time etc.); and

(b) greater exposure to expediting expenses or ICW[1] to mitigate these exposures, albeit often with these being sub limited. All stakeholders faced insured and uninsured exposures.

Per fig 1 as below, we suggest Insurers can expect:

Early market stress → PD cost inflation dominates

Mid-cycle disruption → BI duration starts to overtake

Large industrial losses → total indemnity often driven more by time than rebuild cost

Figure 1: Cost inflation v delay

Key takeaways

Unit price inflation increases claim severity.

Lead time inflation increases claim duration.

In major losses they are positively correlated and compounding.

For complex industrial risks, delay impact typically dominates total indemnity escalation.

Advice: review, proactive, supply chain options.

Complex Claims advice is:

Underwriting & Risk Structuring

• Review declared values adequacy under inflation stress

• Re‑evaluate maximum indemnity periods for supply‑chain critical risks

• Stress‑test catastrophe surge pricing scenarios

• Identify single‑source equipment dependencies

Claims Strategy & Loss Mitigation

• Prioritise programme acceleration over marginal cost negotiation

• Secure early contractor and OEM engagement

• Deploy interim operational solutions to protect revenue

• Apply dynamic reserving linked to delay exposure

______________________________________________________________________________________________________

Insight: In systemic disruption events, duration risk is now a primary driver of insurer loss volatility.

_______________________________________________________________________________________________________

If you would like to discuss any of the implications of this with our Middle East or London team, please contact:

Adam Humphrey ahumphrey@complexclaims.partners

Alan Purbrick apurbrick@complexclaims.partners

[1] Increased Cost of Working